The Canadian real estate market is diverse and dynamic, shaped by regional economic conditions, population growth, and evolving buyer preferences. Major cities like Toronto, Vancouver, Montreal, and Calgary remain popular centres due to their growing job markets, cultural significance, and lifestyle amenities. These urban hubs are attractive to both domestic buyers and international investors, driving demand for various types of housing. In recent years, cities such as Ottawa, Edmonton, Halifax, and Kelowna have also gained traction as more Canadians seek affordable alternatives outside the pricier metropolitan areas.

When it comes to housing types, single-family detached homes have traditionally been the most sought-after, particularly in suburban areas. However, due to rising home prices and limited supply in major cities, there’s been a growing interest in condominiums and townhouses — especially among first-time buyers and downsizers. Purpose-built rental apartments have also surged in popularity, driven by increasing rental demand and investors seeking long-term returns. In smaller communities, semi-detached homes and bungalows remain popular for those seeking more space at relatively lower prices. This blend of housing options reflects Canada’s evolving real estate landscape, balancing affordability challenges with the desire for homeownership.

Canadian Housing Demand

Housing demand in Canada remains strong, driven by a mix of population growth, immigration, and shifting economic factors. Despite recent adjustments to immigration policies aimed at curbing the strain on housing and infrastructure, the influx of newcomers continues to support demand, particularly in urban centers like Toronto, Vancouver, and Montreal. Rising interest rates have tempered some purchasing power, but many buyers are still active, either re-entering the market in anticipation of future rate cuts or seeking more affordable housing options in smaller cities. Additionally, rental demand has surged due to the affordability gap in homeownership, pushing more people toward long-term renting. With a growing population and limited housing supply, the demand for both rental units and entry-level homes remains high, adding pressure to an already tight market.

Several factors have shaped the demand for housing in Canada during 2024 and into 2025. A couple of the most expected reasons are the interest rates and the affordability. The Bank of Canada’s monetary policies have significantly impacted borrowing costs. Even though the interest rates were cut in the middle of 2024, leading to a consequent boost in home sales in the last quarter of 2024, the affordability of homes in several urban centres including Toronto and Vancouver, remains challenging. Even with new listings continually being assimilated into the market, the affordability and the availability challenges remain significant.

Amongst other reason, economic challenges, including rising living costs, have intensified financial hardships for many Canadians. This persistent demand, coupled with government policies and market conditions, directly influences the rate of new housing starts across the country.

New Housing Starts in Canada

The demand for housing is a key driver of housing starts in Canada, influenced by factors such as population growth, employment opportunities, affordability, and government policies. Cities experiencing high immigration and job market expansion often see increased housing demand, prompting developers to build more homes. Lower interest rates and incentives for buyers and builders can further stimulate construction, while high rental demand encourages purpose-built rental projects. Investor activity also plays a role, as speculation can drive or slow new developments. The balance between demand and supply determines market stability, influencing affordability and future housing trends. The supply side of the housing market has experienced notable shifts:

- Monthly Fluctuations: In December 2024, housing starts in Canada decreased by 13% compared to November, according to the Canada Mortgage and Housing Corporation (CMHC). The seasonally adjusted annualized rate fell from 267,140 units in November to 231,468 units in December, primarily due to reductions in both multiple-unit and single-family detached urban homes.

- Yearly Trends: Despite the monthly decline, housing starts for the entire year of 2024 increased by 2% compared to 2023, propelled by historically high levels of rental construction. However, pre-construction sales for one- and two-bedroom condominiums in major cities like Toronto reached record lows, hindering the funding needed for new construction and potentially exacerbating the supply-demand mismatch in the housing market.

- Regional Variations: Year-to-date housing starts from January to December 2024 increased by 15% in Montréal compared to 2023, reflecting a recovery from historically low levels. In contrast, Vancouver and Toronto experienced declines of 15% and 20%, respectively, remaining below 2023’s historically high levels.

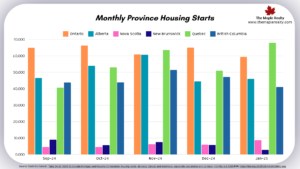

Housing Start Trends

Despite strong demand in key urban centers, housing starts have struggled to keep pace due to affordability challenges, high borrowing costs, and pre-construction condo sales falling short of expectations. A comparison of the housing starts in few of the provinces is shown along with the yearly trend of housing starts in Canada.

Here are a few trends on the housing starts for the Canadian Real Estate Market (seasonally adjusted data).

- Since September 2024, Ontario has seen significant number of housing starts. These numbers are majorly attributed to Toronto, followed by Ottawa. In comparison to 2024, January 2025 saw a drop of 41% in the Toronto starts.

- End of 2024, Quebec has seen an increasing growth in the number of housing starts. 2025 so far has seen more than 100 new housing starts in Montreal, reflecting an over 15% increase yea-over-year (YoY).

- November 2024 saw a number of housing starts , almost matching Ontario in the month, however still less than Quebec.

- As we discussed, the urban hubs have the highest demand and therefore, respective provinces do end up seeing significant construction to balance that.

- High demand and rising prices in British Columbia are reflected in both housing costs and new housing starts. Vancouver experienced a jump of more than 36% YoY for new units started.

- Canada as a whole, saw a month-over-month (MoM) jump of around 240k units. This remains slightly under the market expectations of 251k units.

- July 2024 saw the most activity in terms of new construction beginnings, closely followed by November, May and February (in that sequence).

- The seasonally adjusted annual rate (SAAR) of rural starts was around 19k units.

In summary, Canada’s housing market in 2024 reflected a complex balance between persistent demand and fluctuating housing starts. The response from developers has been encouraging, with notable increases in housing starts in cities like Montreal, while Toronto and Vancouver experienced slowdowns due to weaker pre-construction sales and higher construction costs. As the market moves into 2025, the trajectory of housing starts will largely depend on interest rate adjustments, government incentives, and the ability of the construction sector to keep pace with growing housing needs. The ongoing supply-demand imbalance remains a critical factor, underscoring the importance of accelerating new builds to support Canada’s evolving real estate landscape.